Shutter z // Shutterstock

IEEPA tariffs overturned: Why billions in refund claims may now be at stake for importers

On February 20, 2026, the U.S. Supreme Court issued a landmark 6–3 decision in Learning Resources, Inc. v. Trump, ruling that the International Emergency Economic Powers Act (IEEPA) does not grant the president authority to impose tariffs. The decision struck down the “fentanyl” tariffs applied to Canada, Mexico, and China, along with the broader “reciprocal” tariffs targeting dozens of additional trading partners, dismantling the legal foundation behind a major portion of the administration’s trade policy, Passport reports.

The financial scale is staggering. According to a U.S. Customs and Border Protection (CBP) declaration filed with the U.S. Court of International Trade, more than 333,000 importers paid approximately $166 billion in duties under the now-invalidated IEEPA tariffs. For businesses that made those payments, the Court’s ruling opens the door to one of the largest tariff recovery efforts in modern U.S. trade history.

But recovering those funds won’t be automatic. The Court ruled the tariffs unlawful, but it didn’t establish a process for returning the money. Importers seeking refunds will need to navigate administrative procedures with U.S. Customs and Border Protection, a reminder that even landmark legal victories can leave complex operational work ahead for companies in global trade.

What the IEEPA Ruling Means for Importers

The International Emergency Economic Powers Act (IEEPA) was designed to give the president broad authority to regulate economic transactions during declared national emergencies. Historically, it has been used for sanctions and financial restrictions. In recent years, however, the law was invoked to impose sweeping tariffs on goods imported from countries including Canada, Mexico, and China.

In Learning Resources, Inc. v. Trump, the Supreme Court drew a clear distinction between regulating trade and taxing it. While IEEPA allows the president to regulate imports during a national emergency, the Court concluded that the statute does not authorize tariffs. Because tariffs function as a form of taxation, the administration had interpreted the law beyond its legal limits.

For importers, it is important to distinguish between the Court’s ruling and the process of recovering duties already paid.

The decision declares the tariffs unlawful and removes the legal justification for billions of dollars in collected duties. However, the Court did not mandate automatic refunds or create a direct mechanism for returning the funds.

Instead, importers must pursue recovery through the administrative framework managed by U.S. Customs and Border Protection. That means identifying affected entries and following the appropriate filing process—whether submitting a CBP Protest or a Post Summary Correction, depending on entry status. Without these proactive steps, refunds may never materialize, and billions of dollars could remain with the U.S. Treasury despite the Court’s ruling.

Where IEEPA Tariff Refunds Stand Now

On March 4, 2026, the U.S. Court of International Trade ordered CBP to liquidate or reliquidate certain import entries without tariffs imposed under IEEPA. The ruling in Atmus Filtration, Inc. v. United States follows the Supreme Court’s determination that IEEPA does not authorize presidential tariff authority and applies broadly to affected importers, not just those who filed lawsuits.

If the order stands, many importers could receive refunds without filing individual claims, particularly for entries that remain unliquidated or not yet final. However, CBP told the court it has continued liquidating entries with IEEPA duties included and has not begun issuing refunds. The agency said each entry will likely require review to confirm whether other duties or compliance issues remain outstanding.

The Justice Department is expected to appeal, leaving the timeline and mechanism for refunds uncertain. While the legal landscape continues to evolve, the operational path to recovering duties still depends on the administrative status of each import entry.

According to reporting from Supply Chain Dive on March 6, 2026, CBP told the U.S. Court of International Trade that it cannot immediately comply with the court’s directive to issue refunds for invalidated IEEPA tariffs due to technical and operational constraints. Officials said roughly $166 billion in duties was collected across about 53 million entries, but the agency’s Automated Commercial Environment (ACE) system is not designed to easily separate IEEPA duties from other tariffs. Manually recalculating those entries could require an estimated 4.4 million labor hours.

The court has given CBP 45 days to develop system updates that could automate the process through ACE. In the meantime, entries continue to be liquidated automatically, often in large batches each Friday, locking in duty calculations that CBP cannot currently isolate. The agency also reported that more than 7,700 refunds have already failed to process because some importers have not yet enrolled in the electronic ACH refund system that replaced paper checks earlier this year.

Determining If Your Brand Is Eligible for IEEPA Tariff Refunds

Following the Supreme Court’s decision, many U.S. importers are evaluating whether they can recover duties paid under IEEPA tariffs. Eligibility hinges on several technical factors, including how shipments were filed with customs and who held legal responsibility for paying duties.

For brands evaluating potential claims, three key questions determine where to start.

1. Confirm Your Brand Is the Importer of Record

The first and most important factor is whether your company is listed as the Importer of Record (IOR).

Generally, only the IOR has the legal standing to pursue refunds from CBP. This party is responsible for duty payments, customs declarations, and regulatory compliance.

To verify this, importers should review CBP Form 7501 (Entry Summary). The organization listed in the Importer of Record field is the party authorized to file refund claims.

For many ecommerce brands, this is straightforward. But in certain fulfillment models, particularly Delivered Duty Paid (DDP) arrangements, the situation can be more complicated. If a supplier, freight forwarder, or third-party logistics provider is listed as the IOR, that entity technically owns the refund claim. Any recovery for the brand would depend on commercial agreements between the parties.

2. Verify Your Shipments Were Subject to IEEPA Tariffs

The Supreme Court ruling only applies to tariffs imposed under IEEPA. Other major tariff programs remain fully in effect.

To determine eligibility, importers should confirm that their shipments were assessed duties tied to IEEPA-related executive orders, including the 2025 “fentanyl-related” border tariffs and broader “reciprocal” tariffs. Look for HTSUS codes in the 9903.01.XX and 9903.02.XX ranges. These are the tariff lines CBP used to assess IEEPA duties. If your entries don’t reference codes in the 9903.01.XX or 9903.02.XX ranges, the duties were likely assessed under a different authority, and those programs were not affected by the ruling. Tariffs that remain in effect include:

- Section 301 tariffs targeting Chinese goods

- Section 232 tariffs on steel and aluminum imports

- Section 122, which allows temporary import surcharges

Duties paid under those programs are not eligible for refunds tied to the IEEPA decision.

3. Review the Timing of Your Imports

Even if your shipments were subject to IEEPA tariffs, eligibility also depends on when the goods entered the United States and the administrative status of the import entry.

Only shipments entered between the start of the IEEPA tariff orders in early 2025 and their termination on February 24, 2026, fall within the potential refund window.

How Importers Can File for IEEPA Tariff Refunds

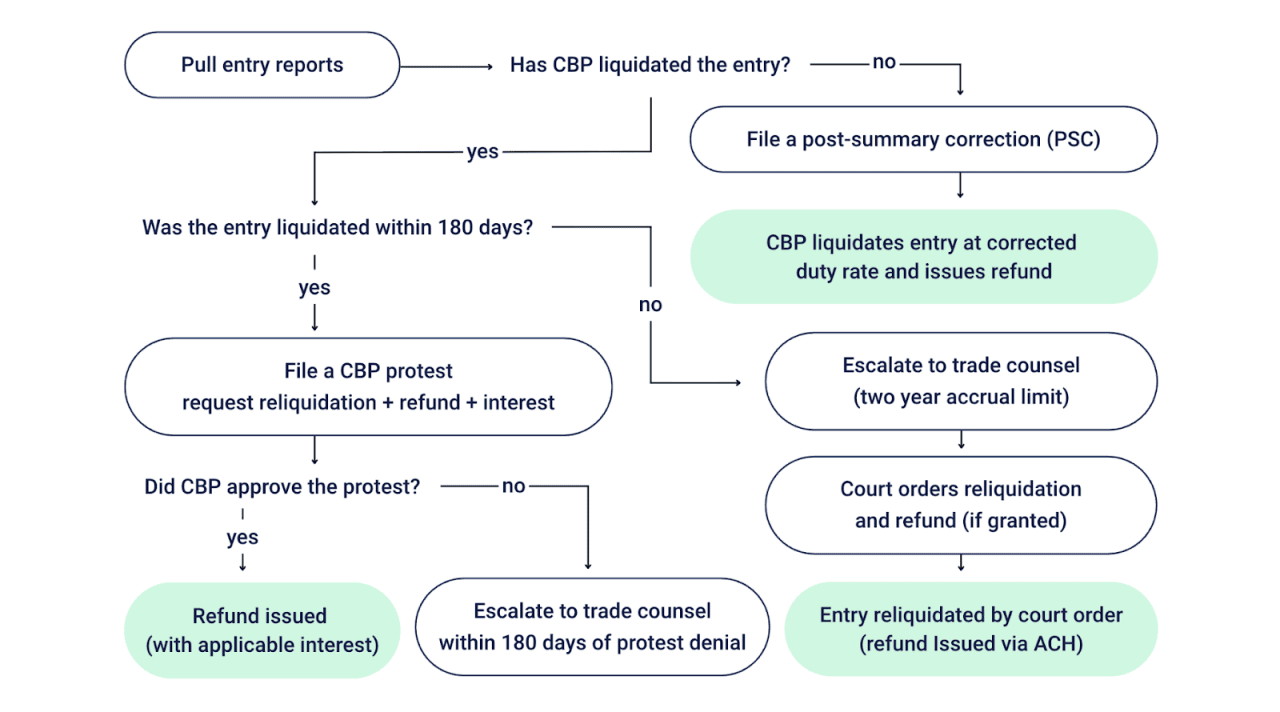

Once a company confirms it may be eligible to pursue refunds, the next step is determining how to file a claim through CBP. The appropriate recovery process depends largely on the liquidation status of each import entry. Whether an entry is still open or already finalized determines which filing path is available.

- Unliquidated Entries: These entries remain open and have not yet been finalized by CBP. Importers can often request corrections using a Post Summary Correction (PSC).

- Liquidated entries: Once an entry is liquidated (typically about 314 days after entry) the duty calculation becomes final. Importers then have 180 days from the liquidation date to file a formal protest.

If the 180-day protest window has already passed, recovering those duties may no longer be possible.

The decision tree below outlines the primary recovery paths available to importers based on the liquidation status of each entry.

Passport

Documentation Needed for Refund Claims

Refund filings must be supported by detailed entry records. Importers typically need documentation such as:

- Entry summaries (CBP Form 7501)

- Duty payment records

- Tariff classifications and Chapter 99 codes

- Documentation identifying the relevant IEEPA tariff lines

Much of this information can be obtained through customs brokers or through the ACE portal, managed by U.S. Customs and Border Protection.

Tracking and Reconciling Refunds

After claims are submitted, refunds must be tracked and reconciled carefully.

Importers should maintain internal records including:

- Affected entry numbers

- Filing dates

- PSC confirmation numbers or protest identifiers

- Expected refund amounts

- Refund receipt status

CBP review timelines can vary, and refund processing may take several months or longer, depending on claim complexity.

What Comes Next: Trade Policy Changes Importers Should Watch

The Supreme Court’s IEEPA ruling creates a historic refund opportunity, but it doesn’t reduce tariff risk. Policymakers retain several other authorities to impose duties—including Section 301, Section 232, and Section 122—and each has been used aggressively in recent years. Importers should expect continued shifts in tariff policy even as the IEEPA tariffs are unwound.

Meanwhile, businesses selling internationally face a new wave of regulatory changes outside the United States. The European Union will eliminate its low-value duty exemption in 2026, applying duties and taxes to all imports regardless of value. Several EU member states are also introducing new customs clearance fees on low-value shipments. For ecommerce brands and global retailers, these changes directly affect landed cost accuracy, margin forecasting, checkout conversion, and the delivery experience for EU customers.

The bottom line: Global trade rules are shifting on multiple fronts simultaneously. The IEEPA decision may close one chapter, but the broader environment demands that brands maintain clear visibility into duties, taxes, and compliance requirements across every market they serve. For companies selling internationally, maintaining clear visibility into duties, taxes, compliance requirements, and customs data is critical.

This story was produced by Passport and reviewed and distributed by Stacker.

![]()